What Is Revenue Cycle Optimization?

Listen to this article

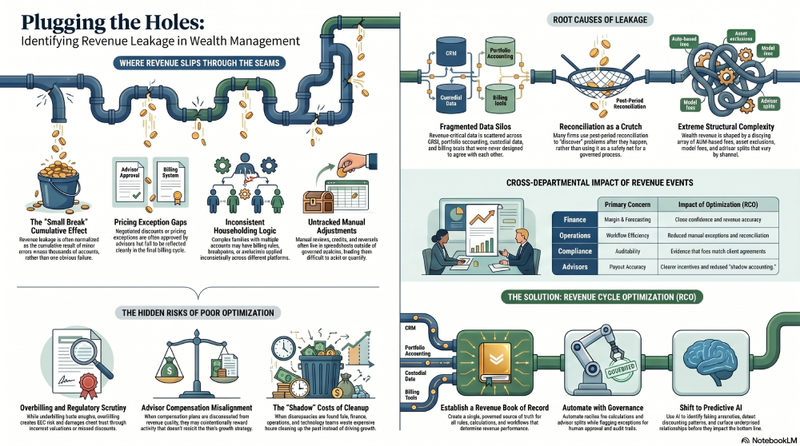

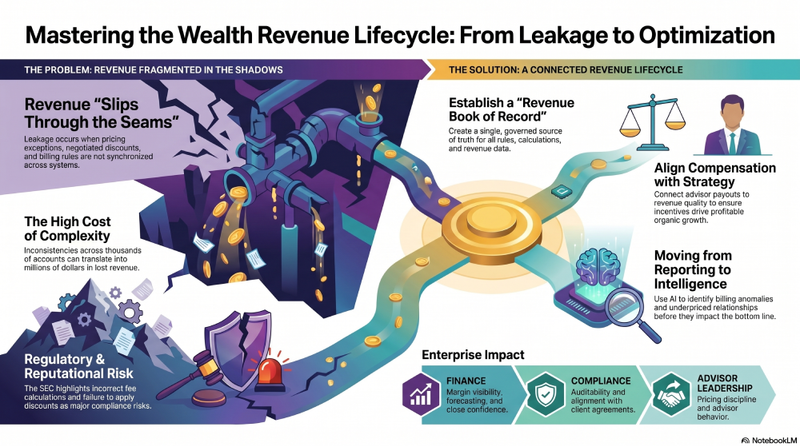

For many wealth management firms, revenue does not fail in one obvious place. It slips through the seams.

A pricing exception is approved but not reflected cleanly in billing. A household has multiple accounts with different fee schedules, breakpoints, exclusions, and negotiated discounts. An advisor compensation plan rewards activity that no longer matches the firm’s growth strategy. Finance discovers discrepancies after the quarter closes. Operations reconciles data across systems that were never designed to agree with each other. Compliance needs evidence that fees were calculated according to client agreements, but the logic lives in a mix of platforms, spreadsheets, manual reviews, and tribal knowledge.

That is the business problem Revenue Cycle Optimization is built to solve in wealth and asset management. It is not simply about getting invoices out faster. It is about managing the full revenue lifecycle with enough accuracy, visibility, control, and intelligence to protect margin, improve advisor behavior, and support profitable organic growth.

What is Revenue Cycle Optimization?

Revenue Cycle Optimization is the process of improving how a wealth or asset management firm prices, calculates, collects, distributes, reconciles, governs, and analyzes revenue across the full revenue lifecycle. In wealth management, it connects fee billing, advisor compensation, client and account data, revenue controls, and performance insights so firms can reduce leakage, improve margins, and make revenue more predictable.

In plain English, it means treating revenue as a connected operating discipline, not a series of disconnected back-office tasks.

For RIAs, broker-dealers, asset managers, and hybrid firms, this matters because revenue is rarely simple. It is shaped by AUM-based fees, tiered schedules, householding logic, asset exclusions, negotiated discounts, model and overlay fees, platform fees, performance fees, advisor splits, grid structures, referrals, bonuses, and special arrangements that vary across clients, advisors, channels, and business lines.

When those inputs are not connected, the firm may still produce revenue. But it may not be producing the revenue it should.

Why Revenue Cycle Optimization matters in wealth management

Wealth revenue is unusually complex

In many industries, revenue cycle management is associated with billing, invoicing, collections, and payment workflows. In wealth and asset management, the concept has to be more specific.

A single client relationship may include taxable accounts, retirement accounts, trusts, managed portfolios, alternative investments, excluded assets, legacy fee arrangements, and negotiated discounts. One household may be billed across multiple accounts or custodians. One advisor may be compensated differently depending on product, channel, tenure, production level, client segment, or practice affiliation.

This complexity creates a basic challenge: the firm needs to know exactly what should be charged, what was charged, what was collected, what should be paid to advisors, and why.

That is harder than it sounds.

The SEC has repeatedly highlighted advisory fee and expense issues as a risk area, including fee calculations that do not match advisory agreements, incorrect valuations, billing in advance or arrears incorrectly, and failures to apply negotiated discounts properly.

For firms managing thousands or millions of accounts, even small inconsistencies can become material. A few basis points of underbilling, overbilling, uncollected fees, excessive discounting, or compensation misalignment can translate into millions of dollars in revenue impact.

Revenue touches more than finance

Revenue Cycle Optimization is often misunderstood as a finance or operations initiative. In wealth management, it cuts across the enterprise.

Finance cares about revenue accuracy, margin visibility, forecasting, and close confidence.

Operations cares about workflow efficiency, exception management, account data, billing rules, and reconciliation.

Technology teams care about integration, scalability, data quality, automation, and system architecture.

Compliance cares about documentation, auditability, fee accuracy, client agreement alignment, and supervisory controls.

Advisor leadership cares about pricing discipline, advisor behavior, client profitability, compensation, and growth.

The same revenue event touches all of them.

A pricing decision made by an advisor can affect billing. Billing affects revenue collection. Revenue collection affects compensation. Compensation affects advisor behavior. Advisor behavior affects client profitability. Client profitability affects firm growth and enterprise value.

Without Revenue Cycle Optimization, each team may optimize its own task while the full system remains inefficient.

Fragmented data weakens revenue performance

Most firms have invested in important systems: CRM, portfolio accounting, billing, compensation, custodial data, reporting, planning tools, data warehouses, and business intelligence platforms.

The problem is not that firms lack technology.

The problem is that revenue-critical data often lives across too many disconnected systems.

Client and household data may sit in one place. Account data in another. Fee schedules somewhere else. Advisor hierarchy and compensation rules in a separate platform. Billing outputs in another workflow. Adjustments and exceptions in spreadsheets. Revenue reports in dashboards that depend on reconciled data after the fact.

This fragmentation makes it difficult to answer simple but essential questions:

- Are we billing every account correctly?

- Are discounts being applied consistently?

- Are we collecting all revenue we are entitled to collect?

- Are advisor compensation plans reinforcing profitable growth?

- Which books, households, segments, or advisors are underperforming revenue potential?

- Where are we losing margin before finance ever sees it?

A firm can have a lot of data and still lack a trustworthy revenue picture.

That is why the idea of a Revenue Book of Record is becoming more important. A Revenue Book of Record gives firms a governed source of truth for the rules, calculations, data, controls, and workflows that determine revenue performance across the lifecycle.

Common problems when firms do not optimize the revenue cycle

1. Revenue leakage becomes normalized

Revenue leakage is often not one dramatic failure. It is the cumulative effect of small breaks across many accounts, teams, and workflows.

Examples include:

- Incorrect fee schedules applied to accounts.

- Negotiated discounts not reflected accurately.

- Assets excluded from billing when they should not be.

- Billing rules applied inconsistently across households.

- Manual adjustments that are not tracked or reviewed.

- Accounts that are not billed on time.

- Credits, reversals, and write-offs that are treated as unavoidable.

In firms with complex account structures, leakage can become part of the operating environment. Everyone knows it exists. Few people can quantify it. Fewer still can identify the root causes quickly enough to prevent it from recurring.

2. Overbilling creates regulatory and reputational risk

Underbilling hurts margin. Overbilling creates a different kind of problem.

If a firm charges clients more than the agreement allows, fails to apply discounts, uses incorrect values, or lacks sufficient records to explain how fees were calculated, the issue can become a compliance, client trust, and reputational problem.

This is why fee billing software and revenue controls are not just efficiency tools. They are part of the firm’s risk infrastructure.

For SEC-registered advisers, fee calculations, disclosures, books and records, and policies and procedures are all relevant to examination readiness. The SEC’s Division of Examinations has specifically issued Risk Alerts to help firms improve systems, policies, and procedures related to compliance obligations.

3. Advisor compensation becomes disconnected from strategy

Advisor compensation is one of the most powerful behavior-shaping tools in wealth management.

But in many firms, compensation plans evolve over time into highly complex structures that are difficult to administer, explain, analyze, and align with strategy.

If compensation plans reward the wrong behavior, the firm may unintentionally encourage excessive discounting, low-margin growth, weak retention discipline, or activity that does not support enterprise priorities.

If compensation calculations are difficult to trust, advisors may spend time questioning payouts instead of growing their books.

If finance and advisor leadership cannot see compensation in relation to revenue quality, client profitability, and growth objectives, the firm loses a major lever for performance improvement.

Revenue Cycle Optimization connects compensation to the broader revenue lifecycle so firms can understand not only what advisors are paid, but how those incentives affect commercial outcomes.

4. Reconciliation becomes the control instead of the safety net

Every firm needs reconciliation. But reconciliation should not be the primary mechanism for discovering revenue problems.

When revenue systems are fragmented, teams often rely on post-period reviews to identify breaks. Finance catches discrepancies. Operations investigates. Technology extracts data. Business leaders wait for answers. Advisors may be pulled into exceptions. By the time the issue is understood, the firm is already cleaning up the past.

That is expensive.

A better approach is to prevent more breaks upstream through automated billing, governed rules, integrated data, exception workflows, and transparent calculation logic.

Reconciliation should confirm confidence, not create it from scratch.

What good Revenue Cycle Optimization looks like

A connected revenue lifecycle

A mature approach to Revenue Cycle Optimization connects the major stages of revenue performance:

- Strategy: Define pricing, fee, compensation, and growth objectives.

- Execution: Operationalize billing, collections, compensation, and workflows.

- Governance: Apply controls, approvals, documentation, and auditability.

- Transparency: Give leaders, advisors, finance, and operations a shared view of revenue performance.

- Intelligence: Use analytics and AI to identify anomalies, revenue potential, leakage, and next-best actions.

- Optimization: Continuously improve pricing discipline, advisor behavior, client profitability, and margin performance.

The key is not simply automating one stage. The key is making the stages work together.

Rules, calculations, and data that can be trusted

Good Revenue Cycle Optimization starts with trust.

That means the firm has clear control over:

- Fee schedules.

- Billing methods.

- Householding logic.

- Account and asset eligibility.

- Discounts and exceptions.

- Advisor hierarchies.

- Compensation rules.

- Revenue adjustments.

- Approval workflows.

- Audit trails.

- Performance reporting.

This is especially important for enterprise wealth firms, where small inconsistencies can scale quickly across large books of business.

Automation with human oversight

Automation is essential, but it should not mean blindly pushing revenue through the system.

The right model combines automation with governance.

Routine calculations should be automated. Known rules should be applied consistently. Exceptions should be flagged. Approvals should be captured. Calculations should be explainable. Leaders should be able to see where revenue is being lost, delayed, adjusted, or placed at risk.

This is where modern revenue management technology can create meaningful value. It helps firms reduce manual work while improving the quality of control.

AI that recommends action, not just reports history

AI has a major role to play in Revenue Cycle Optimization, but only when it is built on reliable data.

In a fragmented environment, AI can produce confident answers from inconsistent inputs. That is not optimization. That is faster confusion.

With a strong revenue foundation, AI can help firms move from backward-looking reporting to forward-looking improvement.

It can identify billing anomalies. Detect advisor discounting patterns. Surface underpriced relationships. Recommend next-best actions. Compare books of business against benchmarks. Highlight clients or households where profitability does not match service intensity. Show where compensation structures may be creating unintended behavior.

That is the real promise of AI in wealth revenue management: not replacing judgment, but giving firms better insight at the moment decisions can still change outcomes.

How wealth firms should approach Revenue Cycle Optimization

The practical starting point is not a massive transformation program. It is a clear diagnostic.

Firms should begin by asking:

- Where do revenue rules live today?

- Which systems calculate, collect, distribute, and report revenue?

- How many manual adjustments occur each cycle?

- How often are fee exceptions reviewed?

- Can we explain every material billing calculation?

- Can we connect advisor compensation to revenue quality?

- Can finance, operations, compliance, and advisor leadership see the same revenue truth?

- Do we know where revenue leakage or revenue potential exists?

From there, firms can prioritize the highest-value areas: fee billing accuracy, revenue reconciliation, advisor compensation alignment, pricing governance, practice profitability, exception management, or executive revenue visibility.

The goal is not perfection on day one.

The goal is to create a more connected, more explainable, and more optimizable revenue lifecycle over time.

Conclusion

Revenue Cycle Optimization gives wealth and asset management firms a clearer way to protect revenue, improve margin, govern complexity, and unlock more organic growth from the business they already have.

For firms ready to connect fee billing, advisor compensation, practice performance, and revenue intelligence in one revenue lifecycle, PureFacts’ PureRevenue Platform is built for that purpose.

FAQs

Why is revenue leakage a major issue for wealth management firms?

Revenue leakage occurs when firms fail to capture revenue they have already earned due to billing errors, manual processes, disconnected systems, or misapplied fee schedules. Even small leaks can significantly impact profitability.

How much revenue do firms typically lose to leakage?

Industry estimates suggest firms can lose between 1% and 5% of annual revenue due to operational inefficiencies and billing inaccuracies.

What causes revenue leakage in wealth and asset management?

Common causes include spreadsheet dependency, disconnected systems, stale fee schedules, manual billing adjustments, advisor discounting, and complex pricing structures.

How does revenue optimization improve profitability?

By reducing leakage, improving pricing governance, automating billing workflows, and aligning advisor compensation with firm strategy, firms can increase EBITDA and improve operating margins.

What is revenue lifecycle optimization?

Revenue lifecycle optimization is the process of improving how a firm prices, calculates, collects, distributes, and analyzes revenue across the entire client and advisor lifecycle.

Why is revenue lifecycle optimization important in wealth management?

It helps firms reduce revenue leakage, improve operational efficiency, strengthen compliance, and increase profitability while supporting scalable growth.

What role does data play in revenue lifecycle optimization?

Clean, centralized data enables accurate billing, compensation calculations, forecasting, compliance reporting, and profitability analysis.

How is revenue cycle optimization different from revenue lifecycle optimization?

Revenue cycle optimization typically focuses more on operational efficiency and collections, while revenue lifecycle optimization covers the broader strategic management of revenue from pricing through analytics and growth.

Why does revenue cycle optimization matter for CFOs?

It improves cash flow, reduces billing errors, strengthens forecasting accuracy, and protects profitability by minimizing revenue leakage.