What Is Billing and Revenue Management?

Listen to this article

For wealth and asset management firms, billing is where commercial strategy becomes financial reality. The firm may have the right client agreements, the right fee schedules, the right advisor compensation plans, and the right growth strategy. But if billing and revenue management are fragmented, the business still loses control at the moment that matters most: when revenue is calculated, collected, distributed, and explained.

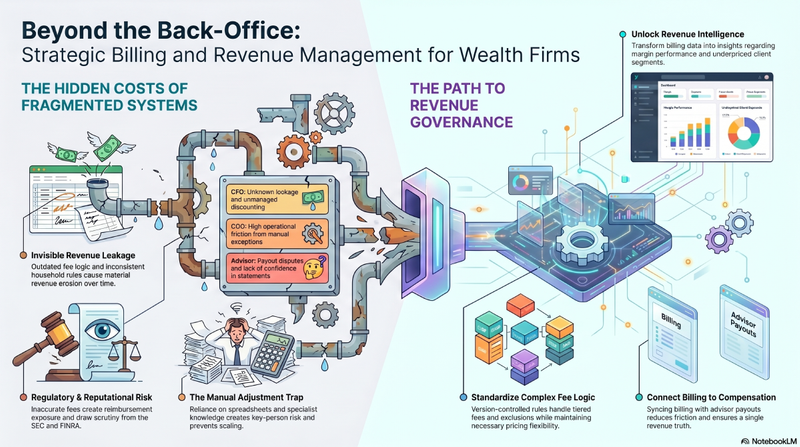

That loss of control rarely announces itself with one obvious failure. It shows up as fee leakage, delayed collections, advisor payout disputes, manual adjustments, recurring credits, client questions, and month-end reconciliations that depend on spreadsheets and institutional memory. In a business built on trust, precision, and margin discipline, billing and revenue management cannot remain a back-office utility. It has to become a governed operating capability.

What is billing and revenue management?

Billing and revenue management is the disciplined process of calculating, collecting, reconciling, distributing, and analyzing revenue across the full wealth management lifecycle. It connects fee billing, client agreements, advisor compensation, accounting, reporting, and governance so firms can protect earned revenue, reduce errors, and scale with confidence.

In wealth management, that means more than sending invoices or running quarterly billing files. It means ensuring that every fee reflects the correct client relationship, asset value, rate schedule, discount, exclusion, household rule, approval, and downstream revenue impact.

Why billing and revenue management matters for wealth firms

Complex fee structures make simple billing impossible

A modern wealth firm may operate across RIAs, broker-dealers, trust companies, family office relationships, custodians, managed accounts, alternative investments, and institutional mandates. Each channel can carry different billing frequencies, valuation methods, breakpoints, minimum fees, negotiated discounts, excluded assets, and legacy exceptions.

The operational challenge is not only calculating the fee. It is applying the right fee logic to the right account, household, advisor, product, and client agreement every time. A single client relationship may include multiple accounts, different asset eligibility rules, tiered pricing, and advisor-specific commercial arrangements. If those rules live in disconnected systems, spreadsheets, CRM notes, or one person’s memory, billing accuracy becomes fragile.

This is where billing and revenue management becomes strategic. It gives firms a way to standardize fee logic, govern exceptions, reconcile source data, and make billing more repeatable without stripping away the pricing flexibility that large wealth and asset management firms need.

Billing decisions affect advisor compensation and behavior

Fee billing does not stop when the client is charged. Revenue flows into advisor compensation, branch performance, channel economics, executive reporting, and margin analysis. If billing data is late, inconsistent, or corrected after the fact, every downstream process becomes harder to trust.

Advisor compensation is especially sensitive. Advisors need confidence that payouts reflect the right clients, assets, credits, adjustments, and plan rules. Finance needs confidence that compensation is based on actual collected or recognized revenue. Leadership needs confidence that incentive structures support growth without encouraging unmanaged discounting or margin erosion.

When billing and compensation are disconnected, firms create unnecessary friction. Advisors challenge statements. Operations teams chase exceptions. Finance reconciles numbers after the fact. Technology teams are asked to patch processes instead of improving the operating model. A connected billing and revenue management approach reduces that friction by treating revenue as one continuous lifecycle, not a series of handoffs.

Revenue accuracy is also a governance issue

In the wealth industry, fees are not just financial transactions. They are client-facing commitments tied to agreements, disclosures, policies, and fiduciary expectations. Regulators have repeatedly emphasized the importance of accurate advisory fee calculations, proper disclosures, and controls that ensure clients are charged in accordance with agreements and stated practices.

That makes billing governance essential. Firms need to demonstrate how fees were calculated, which data was used, which rule was applied, when exceptions were approved, and how adjustments were handled. The more complex the firm, the more important that audit trail becomes.

Strong billing and revenue management gives operations, finance, compliance, and technology teams a shared framework for control. It helps firms move from periodic clean-up to continuous visibility, from manual review to governed exception management, and from “we think this is right” to “we can explain and prove it.”

Common problems when billing and revenue management is weak

The symptoms of weak billing and revenue management are familiar to most wealth firms. The challenge is that they often look like normal operating noise until the financial impact is measured.

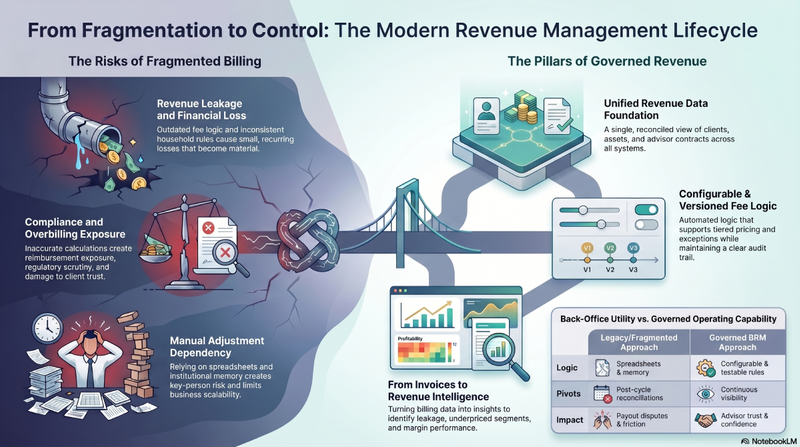

One common problem is revenue leakage from outdated or inconsistent fee logic. A client agreement changes, but the billing setup does not. A breakpoint should apply, but the household structure is wrong. A negotiated discount is approved, but the rule is not reflected consistently across billing, reporting, and compensation. Each issue may be small. Across thousands of accounts and billing cycles, the impact can become material.

Another problem is overbilling risk. Firms often focus on lost revenue, but charging clients too much can be even more damaging. Overbilling creates reimbursement exposure, client trust issues, compliance scrutiny, and reputational risk. A strong revenue management process protects the firm from both underbilling and overbilling.

A third issue is manual adjustment dependency. Many billing teams rely on spreadsheets, offline approvals, exception trackers, or specialist knowledge to get through each cycle. These workarounds can keep the business moving, but they create key-person risk and limit scalability. As firms grow, acquire books, launch new pricing models, or add channels, manual processes become more expensive and less reliable.

Data reconciliation is another recurring problem. Billing depends on account data, asset values, custodial feeds, security classifications, client structures, advisor assignments, fee schedules, and agreement terms. If those inputs are not synchronized, every billing cycle becomes a reconciliation exercise. Teams spend time proving the number instead of improving the process.

Finally, weak billing and revenue management limits executive visibility. CFOs may know total revenue, but not how much is being lost through leakage, delayed collection, unmanaged discounting, recurring credits, or operational exceptions. COOs may know the team is overloaded, but not which processes are creating the most friction. Technology leaders may know systems are fragmented, but not which integration gaps carry the highest financial risk.

What good billing and revenue management looks like

Good billing and revenue management starts with a clear operating principle: revenue should be governed from agreement to insight.

That requires more than automating invoice production. A strong model connects the data, rules, workflows, controls, and reporting that determine how revenue is created, captured, distributed, and analyzed.

1. A trusted revenue data foundation

The firm needs a reliable view of clients, accounts, households, assets, products, advisors, fee schedules, contracts, exceptions, credits, and compensation rules. This does not mean every legacy system disappears. It means revenue-critical data is governed, reconciled, and usable for calculation, reporting, and audit.

2. Configurable fee logic that reflects real-world complexity

Wealth firms need flexibility. They need to support tiered fees, breakpoints, minimums, exclusions, negotiated pricing, prorations, arrears and advance billing, household relationships, and exceptions. But flexibility without governance creates risk. The goal is fee logic that is configurable, version-controlled, testable, and explainable.

3. Connected billing, collection, and compensation workflows

Revenue should not fracture as it moves from client billing to collections, accounting, advisor compensation, and reporting. A strong operating model connects these workflows so changes in one area do not create downstream confusion. When billing and compensation share a consistent revenue truth, firms reduce disputes and improve confidence.

4. Automated controls and exception management

Automation should do more than increase speed. It should strengthen control. Leading firms use structured workflows for approvals, adjustments, credits, write-offs, and exception reviews. They preserve audit trails, reduce manual interpretation, and make recurring issues visible enough to fix at the root.

5. Revenue intelligence for better decisions

The best billing and revenue management programs do not stop at accuracy. They create intelligence. Leaders should be able to see where revenue is leaking, where discounts are concentrated, which fee models are performing, which client segments are underpriced, and which operational breaks are recurring. That turns billing from a back-office process into a source of commercial insight.

How to approach billing and revenue management

The right first step is usually not a wholesale replacement project. It is a practical assessment of the revenue lifecycle.

Firms should map how revenue moves from client agreement to fee setup, account data, asset valuation, calculation, invoice or debit, collection, adjustment, accounting, advisor compensation, reporting, and compliance review. The goal is to identify where rules are interpreted manually, where data is reconciled late, where exceptions accumulate, and where the firm lacks evidence behind the final number.

From there, firms can prioritize the areas with the highest risk and return. For some, that may be automating complex fee billing. For others, it may be connecting billing and compensation, reducing manual adjustments, improving householding accuracy, strengthening audit readiness, or building better executive visibility into leakage and margin performance.

Technology matters, but the strategy matters more. The best approach is not to digitize every existing workaround. It is to create a more controlled revenue lifecycle that supports growth, pricing innovation, advisor trust, client transparency, and financial performance.

Billing and revenue management is now a growth capability

For wealth and asset management firms, billing and revenue management is no longer just an operational necessity. It is the infrastructure that protects earned revenue, supports advisor confidence, improves governance, and gives leadership a clearer view of performance.

Firms that modernize this capability can reduce leakage, prevent costly errors, accelerate reconciliation, and scale more confidently. More importantly, they can turn revenue from a collection of disconnected processes into a controllable, optimizable system.

PureFacts helps wealth and asset management firms connect complex fee billing, advisor compensation, and revenue intelligence so billing and revenue management becomes a measurable advantage across the full revenue lifecycle.